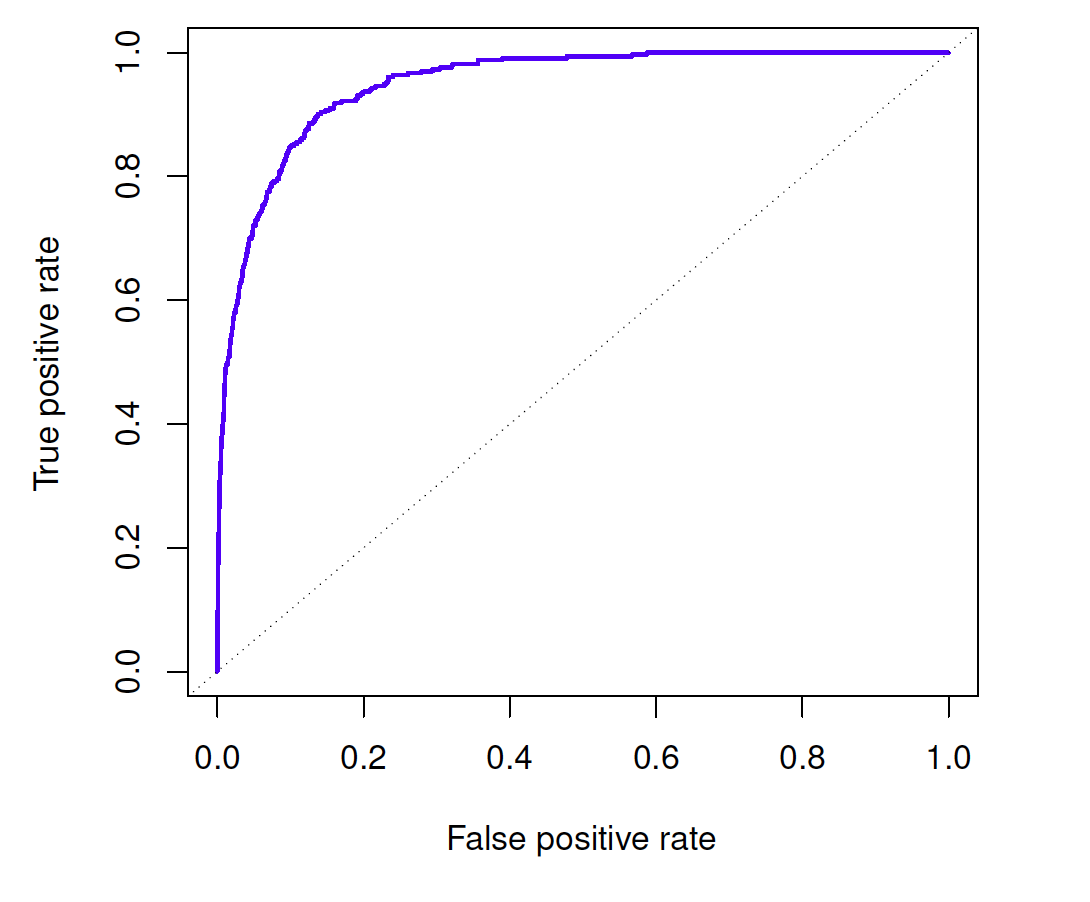

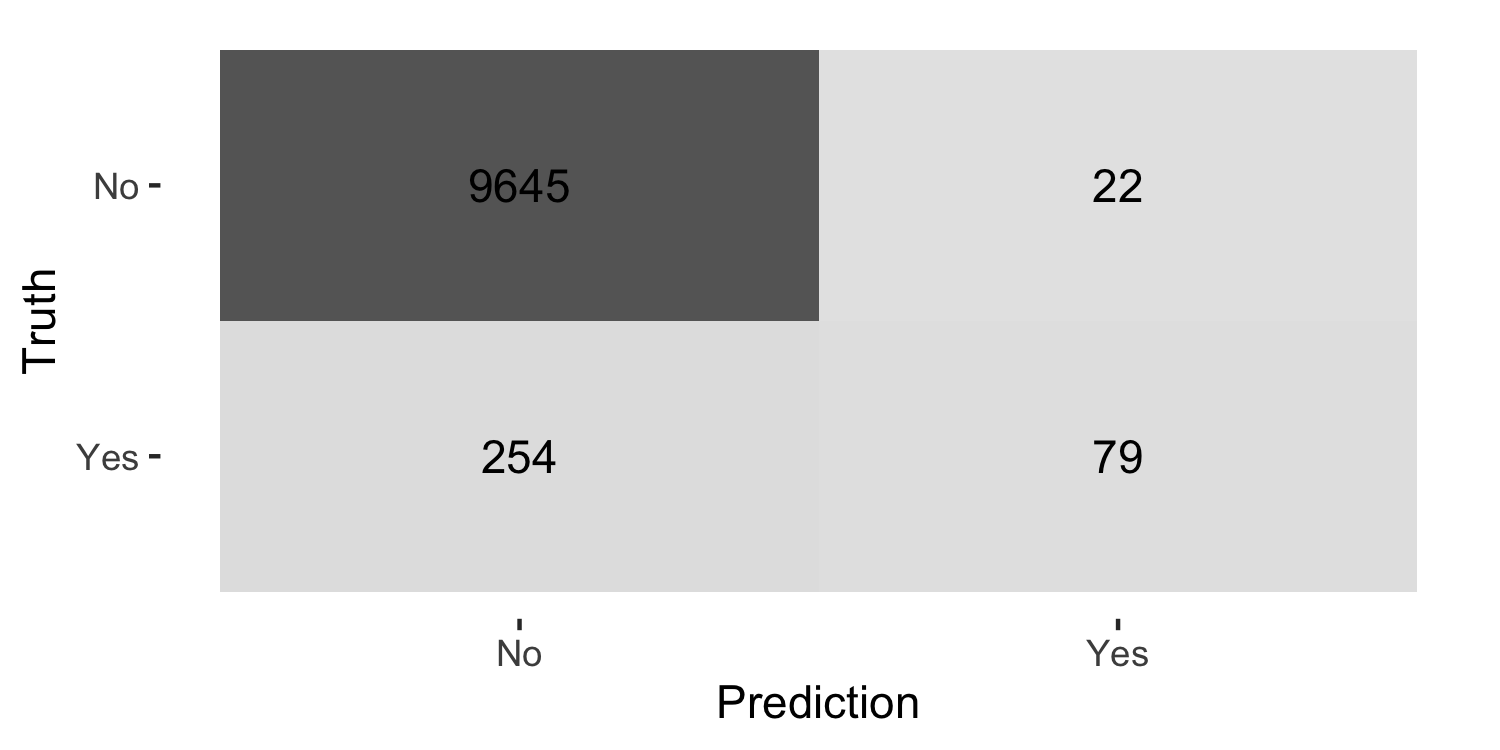

class: center, middle, inverse, title-slide # Logistic regression, LDA, QDA - Part 2 ### Dr. D’Agostino McGowan --- layout: true <div class="my-footer"> <span> Dr. Lucy D'Agostino McGowan <i>adapted from slides by Hastie & Tibshirani</i> </span> </div> --- ## <i class="fas fa-laptop"></i> `LDA` - Go to the [sta-363-s20 GitHub organization](https://github.com/sta-363-s20) and search for `appex-02-lda` - Clone this repository into RStudio Cloud --- <!-- --> * `\(\mu_1 = -1.5\)` * `\(\mu_2 = 1.5\)` * `\(\pi_1=\pi_2=0.5\)` * `\(\sigma^2=1\)` -- * typically we don't know the **true** parameters, we just use our training data to estimate them --- ## Estimating parameters `$$\hat{\pi}_k = \frac{n_k}{n}$$` -- `$$\hat{\mu}_k = \frac{1}{n_k}\sum_{i:y_i=k}x_i$$` -- $$ `\begin{align} \hat{\sigma}^2 &= \frac{1}{n-K}\sum_{k=1}^K\sum_{i:y_i=k}(x_i-\hat{\mu_k})^2\\ &=\sum_{k=1}^K\frac{n_k-1}{n-K}\hat\sigma^2_k \end{align}` $$ -- `$$\hat{\sigma}_k^2= \frac{1}{n_k-1}\sum_{i:y_i=k}(x_i-\hat{\mu}_k)^2$$` --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` ```r df %>% group_by(y) %>% summarise(n = n()) %>% mutate(pi = n / sum(n)) ``` ``` ## # A tibble: 3 x 3 ## y n pi ## <dbl> <int> <dbl> ## 1 1 5 0.333 ## 2 2 5 0.333 ## 3 3 5 0.333 ``` --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` .pull-left[ ```r df %>% * group_by(y) %>% summarise(n = n()) %>% mutate(pi = n / sum(n)) ``` ``` ## # A tibble: 3 x 3 ## y n pi ## <dbl> <int> <dbl> ## 1 1 5 0.333 ## 2 2 5 0.333 ## 3 3 5 0.333 ``` ] .pull-right[ * `group_by()`: do calculations on groups ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` .pull-left[ ```r df %>% group_by(y) %>% * summarise(n = n()) %>% mutate(pi = n / sum(n)) ``` ``` ## # A tibble: 3 x 3 ## y n pi ## <dbl> <int> <dbl> ## 1 1 5 0.333 ## 2 2 5 0.333 ## 3 3 5 0.333 ``` ] .pull-right[ * `group_by()`: do calculations on groups * `summarise()`: reduce variables to values ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 |5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` .pull-left[ ```r df %>% group_by(y) %>% summarise(n = n()) %>% * mutate(pi = n / sum(n)) ``` ``` ## # A tibble: 3 x 3 ## y n pi ## <dbl> <int> <dbl> ## 1 1 5 0.333 ## 2 2 5 0.333 ## 3 3 5 0.333 ``` ] .pull-right[ * `group_by()`: do calculations on groups * `summarise()`: reduce variables to values * `mutate()`: add new variables ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 |5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` .pull-left[ ```r df %>% group_by(y) %>% summarise(n = n()) %>% mutate(pi = n / sum(n)) ``` ] .pull-right[ * `group_by()`: do calculations on groups * `summarise()`: reduce variables to values * `mutate()`: add new variables ] .question[ How do we pull `\(\pi_k\)` out into their own R object? ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 |5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` ```r df %>% group_by(y) %>% summarise(n = n()) %>% mutate(pi = n / sum(n)) %>% * pull(pi) -> pi ``` .question[ How do we pull `\(\pi_k\)` out into their own R object? ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 |5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\pi}_k = \frac{n_k}{n}$$` ```r pi ``` ``` ## [1] 0.3333333 0.3333333 0.3333333 ``` .question[ How do we pull `\(\pi_k\)` out into their own R object? ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\mu}_k = \frac{1}{n_k}\sum_{i:y_i=k}x_i$$` ```r df %>% group_by(y) %>% * summarise(mu = mean(x)) ``` ``` ## # A tibble: 3 x 2 ## y mu ## <dbl> <dbl> ## 1 1 -1.46 ## 2 2 1.5 ## 3 3 3.54 ``` --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{\mu}_k = \frac{1}{n_k}\sum_{i:y_i=k}x_i$$` ```r df %>% group_by(y) %>% summarise(mu = mean(x)) %>% * pull(mu) -> mu ``` --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 $$ `\begin{align} \hat{\sigma}^2 =\sum_{k=1}^K\frac{n_k-1}{n-K}\hat\sigma^2_k \end{align}` $$ .small[ ```r df %>% group_by(y) %>% summarise(var_k = var(x), n = n()) %>% mutate(v = ((n - 1) / (sum(n) - 3)) * var_k) %>% summarise(sigma_sq = sum(v)) ``` ``` ## # A tibble: 1 x 1 ## sigma_sq ## <dbl> ## 1 1.47 ``` ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 $$ `\begin{align} \hat{\sigma}^2 =\sum_{k=1}^K\frac{n_k-1}{n-K}\hat\sigma^2_k \end{align}` $$ ```r df %>% group_by(y) %>% summarise(var_k = var(x), n = n()) %>% mutate(v = ((n - 1) / (sum(n) - 3)) * var_k) %>% summarise(sigma_sq = sum(v)) %>% pull(sigma_sq) -> sigma_sq ``` --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\delta_k(x) = x \frac{\mu_k}{\sigma^2}-\frac{\mu_k^2}{2\sigma^2}+\log(\pi_k)$$` * Let's predict the class for `\(x = 2\)` ```r x <- 2 x * (mu / sigma_sq) - mu^2 / (2 * sigma_sq) + log(pi) ``` ``` ## [1] -3.8155857 0.1795063 -0.5436021 ``` -- .question[ Which class should we give this point? ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\delta_k(x) = x \frac{\mu_k}{\sigma^2}-\frac{\mu_k^2}{2\sigma^2}+\log(\pi_k)$$` * Let's predict the class for `\(x = 6\)` ```r x <- 6 x * (mu / sigma_sq) - mu^2 / (2 * sigma_sq) + log(pi) ``` ``` ## [1] -7.796499 4.269486 9.108750 ``` -- .question[ Which class should we give this point? ] --- ## From the discriminant score to probabilities We can turn `\(\hat{\delta}_k(x)\)` into estimates for class probabilities -- `$$\hat{P}(Y=k|X=x)=\frac{e^{\hat{\delta}_k(x)}}{\sum_{l=1}^Ke^{\hat{\delta}_l(x)}}$$` -- * Classifying the largest `\(\hat{\delta}_k(x)\)` is the same as classifying to the class with the largest `\(\hat{P}(Y=k|X=x)\)` -- * For `\(K=2\)`: * classify to 2 if `\(\hat{P}(Y=2|X=x)\ge 0.5\)` * classify to 1 otherwise --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 `$$\hat{P}(Y=k|X=x)=\frac{e^{\hat{\delta}_k(x)}}{\sum_{l=1}^Ke^{\hat{\delta}_l(x)}}$$` * Let's get the posterior probability of each class for `\(x = 6\)` .small[ ```r x <- 6 d <- x * (mu / sigma_sq) - mu^2 / (2 * sigma_sq) + log(pi) exp(d) / sum(exp(d)) ``` ``` ## [1] 4.515655e-08 7.850755e-03 9.921492e-01 ``` ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 * There is a function to do this in R called `lda()` in the **MASS** package .small[ ```r *library(MASS) model <- lda(y ~ x, data = df) ``` ] --- ## Estimating parameters (in R!) x | -1.6| 0.2| -0.9| -2.0| -3.0| 1.9| 1.2| 2.2| 2.7| -0.5 | 1.8 | 3.3 | 5.0 | 3.4 | 4.2 --|--|--|--|--|--|--|--|--|--|--|--|--|--|--|-- y | 1 | 1 | 1| 1| 1| 2|2|2|2|2|3|3|3|3|3 * There is a function to do this in R called `lda()` in the **MASS** package .small[ ```r library(MASS) model <- lda(y ~ x, data = df) *predict(model, newdata = data.frame(x = 6)) ``` ``` ## $class ## [1] 3 ## Levels: 1 2 3 ## ## $posterior ## 1 2 3 ## 1 4.515655e-08 0.007850755 0.9921492 ## ## $x ## LD1 ## 1 3.968523 ``` ] --- ## <i class="fas fa-laptop"></i> `LDA` - Go to the [sta-363-s20 GitHub organization](https://github.com/sta-363-s20) and search for `appex-02-lda` - Clone this repository into RStudio Cloud - Complete the exercises - **Knit, Commit, Push** --- ## Linear discriminant analysis `\(p>1\)`  * When `\(p>1\)` the density takes on the **multivariate normal** density `$$f(x) = \frac{1}{(2\pi)^{p/2}|\mathbf\Sigma|^{1/2}}e^{-\frac{1}{2}(x-\mu)^T\mathbf\Sigma^{-1}(x-\mu)}$$` --- ## Linear discriminant analysis `\(p>1\)`  * The **discriminant function** is now `$$\delta_k(x)=x^T\mathbf\Sigma^{-1}\mu_k-\frac{1}{2}\mu_k^T\mathbf\Sigma^{-1}\mu_k+\log\pi_k$$` * This is still a linear function! --- ## Example `\(p = 2\)`, `\(K = 3\)`  * Here `\(\pi_1 = \pi_2 = \pi_3 = 1/3\)` * The dashed lines the Bayes decision boundaries * If they were known, they would yield the fewest misclassification errors, among all possible classifiers. --- ## LDA on Credit Data | True Default (No) | True Default (Yes) | Total -|------------------|---------------------|----- **Predicted Default (No)** | 9644 | 252| 9895 **Predicted Default (Yes)** | 23 | 81 | 104 **Total** | 9667 | 333 | 10000 .question[ What is the misclassification rate? ] -- * `\(\frac{23 + 252}{10000}\)` errors - `\(2.75\%\)` misclassification -- .question[ Since this is **training error** what is a possible concern? ] -- * This could be **overfit** --- ## LDA on Credit Data | True Default (No) | True Default (Yes) | Total -|------------------|---------------------|----- **Predicted Default (No)** | 9644 | 252| 9895 **Predicted Default (Yes)** | 23 | 81 | 104 **Total** | 9667 | 333 | 10000 * `\(\frac{23 + 252}{10000}\)` errors - `\(2.75\%\)` misclassification * ~~This could be **overfit**~~ * Since we have a **large n** and **small p** ( `\(n = 10,000\)`, `\(p = 4\)` ) we aren't too worried about overfitting --- ## LDA on Credit Data | True Default (No) | True Default (Yes) | Total -|------------------|---------------------|----- **Predicted Default (No)** | 9644 | 252| 9895 **Predicted Default (Yes)** | 23 | 81 | 104 **Total** | 9667 | 333 | 10000 * `\(\frac{23 + 252}{10000}\)` errors - `\(2.75\%\)` misclassification -- .question[ What would the error rate be if we classified to the _prior_, `No` default? ] -- * `\(333/10000\)` - `\(3.33\%\)` --- ## LDA on Credit Data | True Default (No) | True Default (Yes) | Total -|------------------|---------------------|----- **Predicted Default (No)** | 9644 | 252| 9895 **Predicted Default (Yes)** | 23 | 81 | 104 **Total** | 9667 | 333 | 10000 * `\(\frac{23 + 252}{10000}\)` errors - `\(2.75\%\)` misclassification * Since we have a **large n** and **small p** ( `\(n = 10,000\)`, `\(p = 4\)` ) we aren't too worried about overfitting * Of the true `No`'s, we make `\(23/9667 = 0.2\%\)` errors; of the true `Yes`'s, we make `\(252/333 = 75.7\%\)` errors! --- ## Types of errors * **False positive rate**: The fraction of truly negative that are classified as positive * **False negative rate**: The fraction of truly positive that are classified as negative -- .question[ What is the false positive rate in the Credit Default example? ] -- * 0.2% -- .question[ What is the false negative rate in the Credit Default example? ] -- * 75.7% --- ## Types of errors * **False positive rate**: The fraction of truly negative that are classified as positive * **False negative rate**: The fraction of truly positive that are classified as negative * The Credit Default table was created by predicting the `Yes` class if `$$\hat{P}(\texttt{Default}|\texttt{Balance, Student})\ge 0.5$$` -- * We can change the two error rates by changing the **threshold** from 0.5 to some other number between 0 and 1 `$$\hat{P}(\texttt{Default}|\texttt{Balance, Student})\ge threshold$$` --- ## Varying the _threshold_  * To reduce the **false negative rate** we may want the threshold to be 0.1 or less --- ## ROC .pull-left[  ] .pull-right[ * A receiver operating characteristic (ROC) curve looks at both simultaneously * The area under the ROC curve (AUC) is sometimes a metric for performance ] -- .question[ Which do you think is better, higher or lower AUC? ] --- ## Let's see it in R .small[ ```r library(MASS) model <- lda(default ~ balance + student + income, data = Default) ``` ] * Use the `lda()` function in R from the **MASS** package --- ## Let's see it in R .small[ ```r library(MASS) model <- lda(default ~ balance + student + income, data = Default) *predictions <- predict(model) ``` ] * Use the `lda()` function in R from the `MASS` package * Get the predicted classes along with posterior probabilities using the `predict()` function --- ## Let's see it in R .small[ ```r library(MASS) model <- lda(default ~ balance + student + income, data = Default) predictions <- predict(model) Default %>% * mutate(predicted_class = predictions$class) ``` ] * Use the `lda()` function in R from the `MASS` package * Get the predicted classes along with posterior probabilities using the `predict()` function * Add the predicted class using the `mutate()` function --- ## Let's see it in R .small[ ```r library(MASS) model <- lda(default ~ balance + student + income, data = Default) predictions <- predict(model) Default %>% mutate(predicted_class = predictions$class) %>% summarise(fpr = * sum(default == "No" & predicted_class == "Yes") / * sum(default == "No"), fnr = * sum(default == "Yes" & predicted_class == "No") / * sum(default == "Yes")) ``` ``` ## fpr fnr ## 1 0.002275784 0.7627628 ``` ] * Use the `summarise()` function to add the false positive and false negative rates --- ## Let's see it in R .small[ ```r library(MASS) *library(tidymodels) model <- lda(default ~ balance + student + income, data = Default) predictions <- predict(model) Default %>% mutate(predicted_class = predictions$class) %>% * conf_mat(default, predicted_class) %>% * autoplot(type = "heatmap") ``` <!-- --> ] --- ## Let's see it in R * `conf_mat()` expects your outcome to be a factor variable ```r library(MASS) *library(tidymodels) model <- lda(default ~ balance + student + income, data = Default) predictions <- predict(model) Default %>% mutate(predicted_class = predictions$class, * default = as.factor(default)) %>% conf_mat(default, predicted_class) %>% autoplot(type = "heatmap") ```